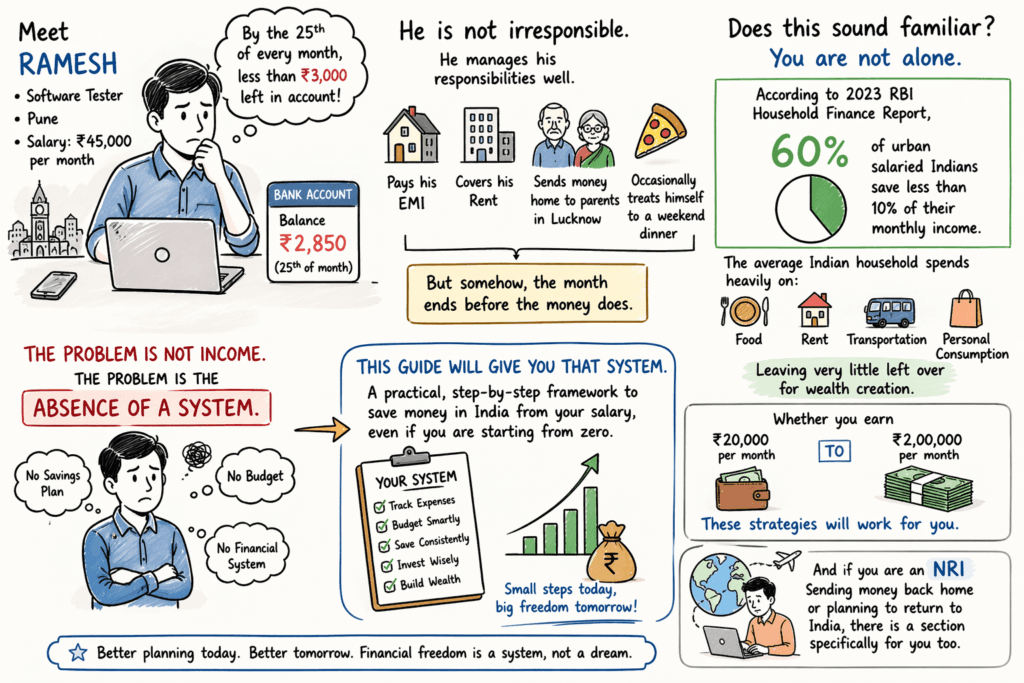

Saving money without a financial foundation is like building a house on sand.

Emergency Fund

An emergency fund is 3 to 6 months of expenses kept in a liquid account. It protects you from unexpected events like job loss or medical emergencies.

Debt Strategy

High interest debt like credit cards and personal loans should be cleared first. Use the avalanche method by paying off the highest interest debt first.

Never stop EPF contributions, as they provide guaranteed returns and employer matching.

Automate Your Savings

Monthly Savings Plan

| Investment Type | Amount | Purpose |

|---|

| Emergency Fund | ₹3,000 | Safety |

| SIP Investment | ₹5,000 | Wealth |

| PPF | ₹2,000 | Retirement |

Start SIPs with beginner guides available on Mint & Print.

The biggest enemy of saving is inconsistency. Automation solves this problem.

Pay Yourself First

Set up automatic transfers on salary day so your savings are deducted before spending begins.

SIP Investment Strategy

A Systematic Investment Plan allows you to invest small amounts regularly. Even ₹500 per month builds long term wealth through compounding.

A ₹5000 monthly SIP over 15 years can grow to ₹25 to ₹30 lakh depending on returns.

Tax Smart Saving

Tax Saving Options

| Section | Investment | Limit |

|---|

| 80C | PPF ELSS EPF | ₹1.5 Lakh |

| 80D | Health Insurance | ₹25,000 |

| 24 | Home Loan Interest | ₹2 Lakh |

Saving money is also about reducing taxes legally.

Section 80C

You can claim deductions up to ₹1.5 lakh through EPF, PPF, ELSS, and other instruments.

Section 80D and Other Benefits

Health insurance premiums and home loan interest provide additional tax benefits.

Old vs New Tax Regime

Choose based on your deductions. Higher deductions favor the old regime, while fewer deductions favor the new regime.

Like every Wealth creator believes in following Principles-

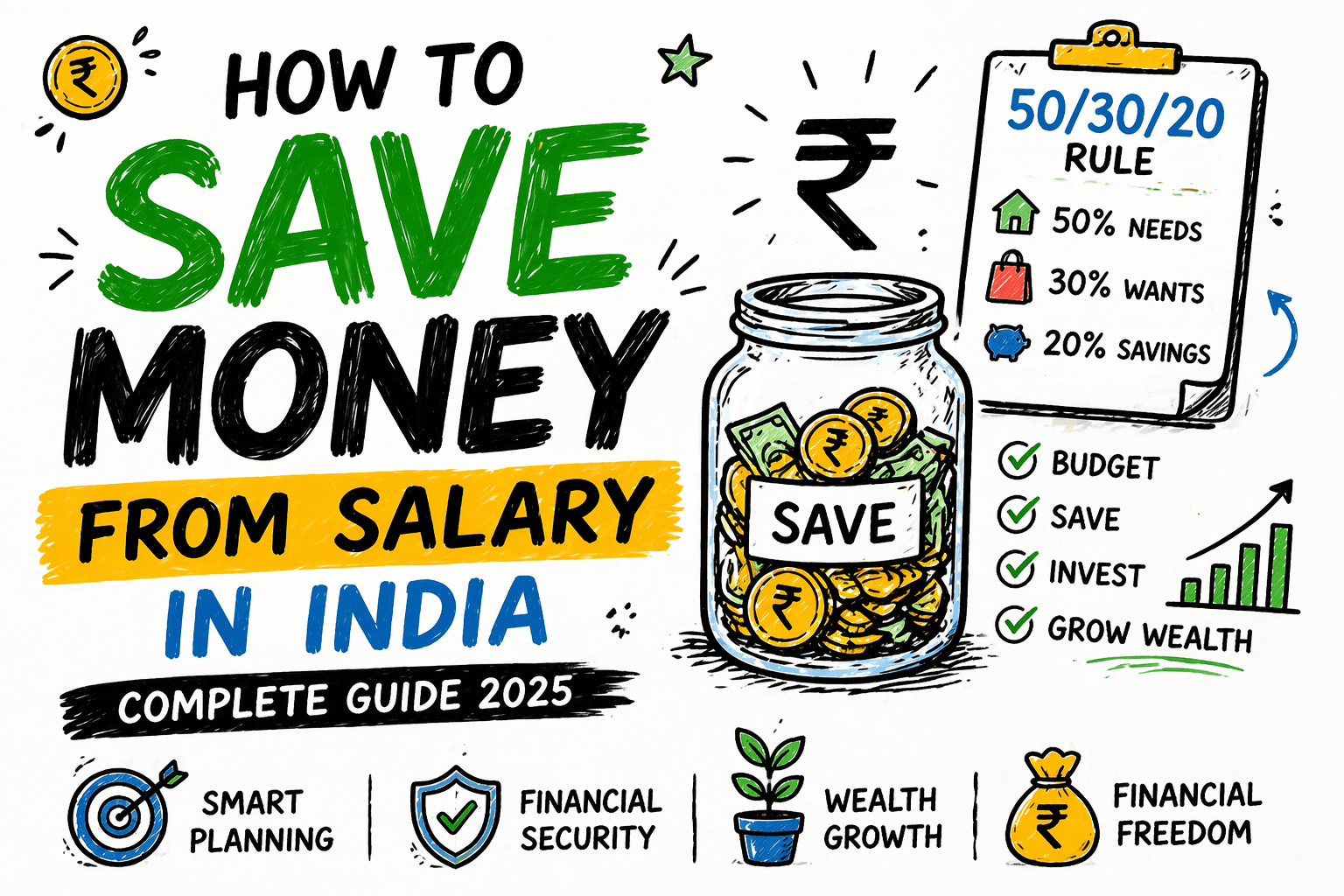

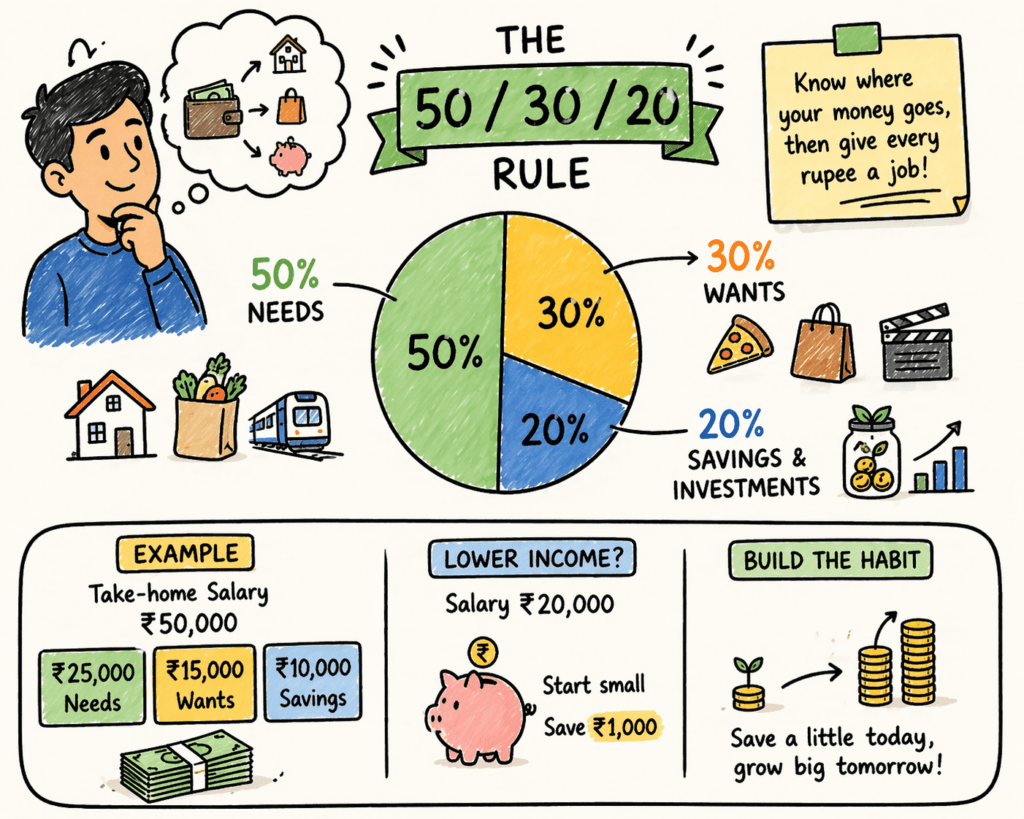

- Saving money in India from salary requires a disciplined approach.

- If you want to save money in India from salary, you must start with budgeting.

- Many people fail to save money in India from salary because they lack a proper system.

- The best way to save money in India from salary is by following the 50 30 20 rule.

- Once you learn how to save money in India from salary, financial stability becomes easier.

Post Comment