Start SIP in India with ₹500 Today — Every Month You Wait Costs You More

SIP & Mutual Funds

How to start SIP with ₹500/month

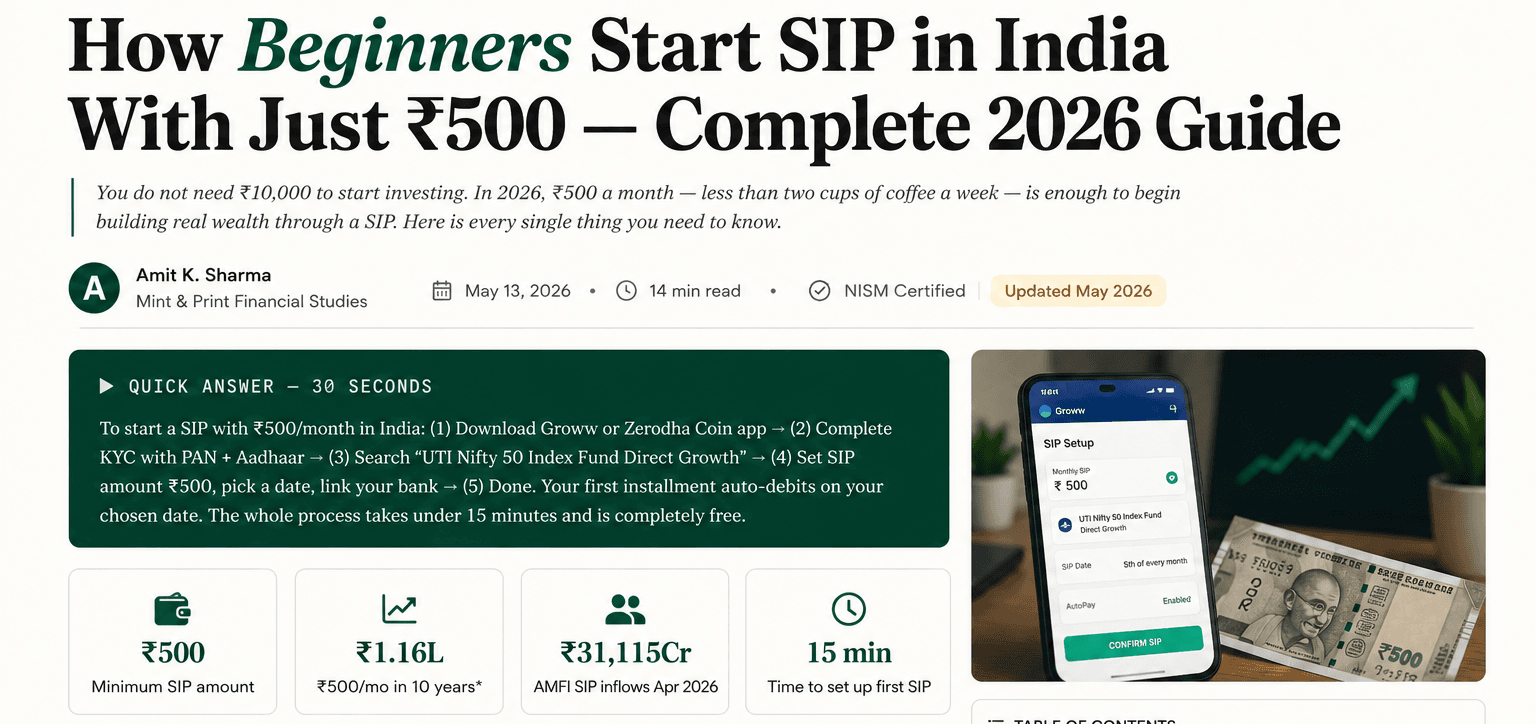

Want to start SIP in India with ₹500? This beginner-friendly 2026 guide explains how SIP investing works, how to choose mutual funds, how to use the Groww app, and common mistakes beginners should avoid. You do not need ₹10,000 to start investing. In 2026, ₹500 a month — less than two cups of coffee a week — is enough to begin building real wealth through a SIP. Here is every single thing you need to know.

Quick Answer — 30 seconds

To start a SIP with ₹500/month in India: (1) Download Groww or Zerodha Coin app → (2) Complete KYC with PAN + Aadhaar → (3) Search "UTI Nifty 50 Index Fund Direct Growth" → (4) Set SIP amount ₹500, pick a date, link your bank → (5) Done. Your first installment auto-debits on your chosen date. The whole process takes under 15 minutes and is completely free.

₹500

Minimum SIP amount

₹1.16L

₹500/mo in 10 years*

₹31,115Cr

AMFI SIP inflows Apr 2026

15 min

Time to set up first SIP

*Assumes 12% annual returns. Not guaranteed. Educational illustration only.

Let me start with something that surprises almost every beginner I speak to: India's mutual fund industry crossed ₹50 lakh crore in total AUM in late 2025. And according to AMFI's official data, average monthly SIP inflows have more than doubled in just three years — from ₹13,000 crore in FY23 to over ₹28,000 crore in FY26. Millions of regular Indians — students, salaried employees, homemakers — are building wealth one ₹500 at a time.

And yet, the number one reason people I meet give for not starting is: "I don't have enough money to invest."

That belief is holding millions of Indians back from one of the most powerful wealth-building habits available to them. This guide is going to demolish it.

1. What Is a SIP — And why to Start SIP in India with ₹500?

A Systematic Investment Plan (SIP) is a method of investing a fixed amount of money into a mutual fund at regular intervals — usually monthly. Think of it exactly like an EMI, except instead of paying a bank for a loan, you are paying your future self.

When you set up a SIP, on the same date every month, your chosen amount is automatically debited from your bank account and invested in your selected mutual fund. You do not have to remember to transfer money. You do not have to decide whether the market is high or low. It just happens.

Now, why does ₹500 matter specifically? Because most Indians have been told they cannot start investing without a large sum. That is simply false in 2026. Most major mutual fund platforms allow SIPs from ₹500/month, and many allow even ₹100/month. The amount is almost irrelevant at the start — what matters is the habit.

The real power is in starting early, not starting big. A ₹500/month SIP started at age 22 beats a ₹5,000/month SIP started at age 32 — because of the extra 10 years of compounding. Time in the market beats money in the market.

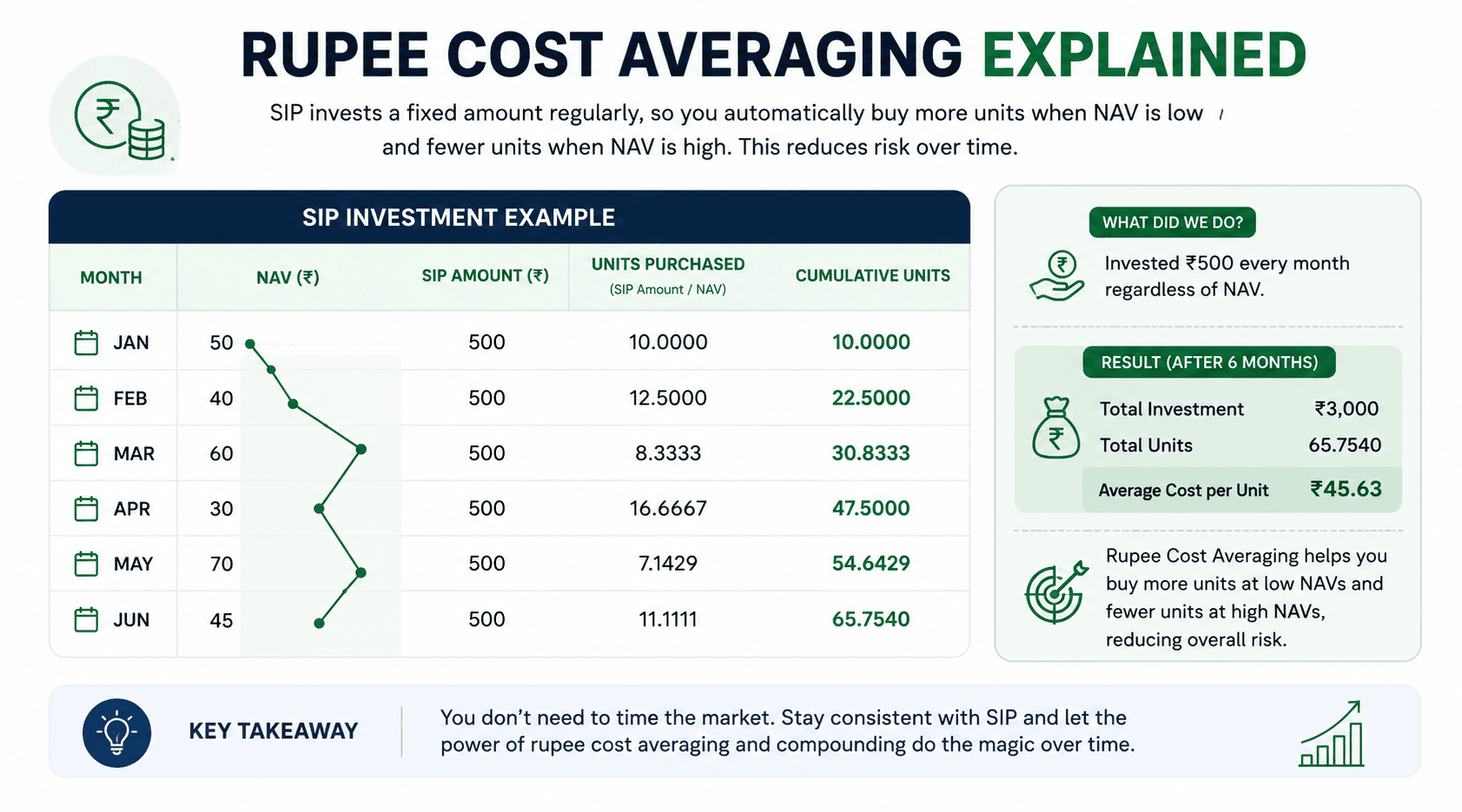

2. How SIP Actually Works: Rupee Cost Averaging Explained

<

This is the part that most SIP guides explain badly, so let me be clear.

When you invest ₹500 into a mutual fund, you do not get a fixed number of shares. You buy units based on the fund's Net Asset Value (NAV) on that day. The NAV changes daily with the market. This is where the magic of Rupee Cost Averaging happens.

Imagine the NAV of your chosen fund across three months:

| Month | NAV (₹) | Investment | Units Purchased |

|---|---|---|---|

| January | 50.00 | ₹500 | 10.00 units |

| February (market fall) | 40.00 | ₹500 | 12.50 units ↑ |

| March (recovery) | 55.00 | ₹500 | 9.09 units |

| Total | Avg ₹47.62 | ₹1,500 | 31.59 units |

Notice what happened in February when the market fell: your ₹500 automatically bought more units. By March, when the market recovered, those extra units gained in value. Your average cost per unit was ₹47.62 — lower than what you'd have paid with a one-time investment. This is Rupee Cost Averaging at work.

Key insight: A market crash during your SIP journey is not a disaster — it is actually an opportunity. You buy more units at lower prices, and when markets recover (which they historically always have), you gain more. This is why SIP is ideal for volatile markets.

3. SIP vs Lump Sum: Which is Better for Beginners?

✅ SIP (Recommended for Beginners)

- Start with as little as ₹500/month

- No need to time the market

- Rupee Cost Averaging reduces risk

- Auto-debit builds investment discipline

- Perfect for salaried/regular income

- Can increase amount anytime

- Pause or stop without penalty

◎ Lump Sum (For Experienced Investors)

- Requires a large amount upfront

- Better when market is clearly undervalued

- Higher returns if timed perfectly

- Higher risk if market falls after investing

- No averaging benefit

- Needs market knowledge to execute well

- Not recommended for beginners

For a beginner investing ₹500 a month, the answer is clear: always start with SIP. The combination of low starting amount, automatic discipline, and built-in risk management through Rupee Cost Averaging makes it the single best entry point for new investors in India.

4. Best SIP Funds for Beginners With ₹500/Month in 2026

This is the question every beginner asks first. Here is my honest answer: for a first-time investor with ₹500/month, a Nifty 50 Index Fund is the safest and smartest choice in 2026.

Not because it gives the highest returns — it doesn't. But because:

- You are investing in India's top 50 companies — no single bad stock can destroy your portfolio

- The expense ratio is ultra-low (around 0.1–0.2%) — you keep more of your returns

- No fund manager risk — it simply tracks the index

- Historical returns of 12–15% over 10+ year periods (not guaranteed, but consistent)

Best for Absolute Beginners

UTI Nifty 50 Index Fund — Direct Growth

Min SIP₹500/month

Expense Ratio~0.18%

5-Year Return (approx)~16% p.a.

Risk LevelModerate

Nifty 50 Index · Passive

Best Low-Cost Alternative

HDFC Index Fund — Nifty 50 Plan Direct Growth

Min SIP₹500/month

Expense Ratio~0.20%

5-Year Return (approx)~15.8% p.a.

Risk LevelModerate

Nifty 50 Index · Passive

Best Flexi Cap Option (After 6 months)

Parag Parikh Flexi Cap Fund — Direct Growth

Min SIP₹1,000/month

Expense Ratio~0.55%

5-Year Return (approx)~20% p.a.

Risk LevelModerate-High

Flexi Cap · Active

Best for Tax Saving (ELSS)

Mirae Asset ELSS Tax Saver Fund — Direct Growth

Min SIP₹500/month

Lock-in Period3 years

Tax BenefitSection 80C

Risk LevelModerate-High

ELSS · Tax Saving · 80C

Direct vs Regular Plans — always choose Direct: When searching for a fund on any app, you will see two versions — "Direct" and "Regular." Always choose Direct. Regular plans pay a commission to distributors, which reduces your returns by 0.5–1% annually. Over 20 years, this seemingly small difference can cost you lakhs of rupees.

5. Step-by-Step: How Beginners Can Start SIP in India with ₹500

")

I will walk you through this on Groww (works identically on Zerodha Coin and Paytm Money). The entire process below assumes you are starting from scratch with no existing account.

-

1

Download Groww and create your account

Download Groww from Google Play or App Store. Open it and tap "Sign Up." Enter your mobile number and email, verify both with OTPs. Groww is free to use and charges no account opening fee.

💡 Alternatively, use Zerodha Coin if you already have a Zerodha demat account — your KYC is already done. -

2

Complete your KYC — takes 5 minutes

Tap "Complete KYC." Enter your PAN card number and date of birth. Then upload a photo of your Aadhaar (both sides) or verify via Digilocker (recommended — faster). Take a selfie for identity verification. SEBI mandates KYC for all mutual fund investments — you cannot skip this step.

⚠️ Your name on PAN and Aadhaar must match exactly. A mismatch will delay KYC approval by 1–2 days. -

3

Link your bank account

Go to Profile → Bank Account → Add Bank. Enter your account number and IFSC code. Groww will verify your account instantly via a small UPI verification or penny deposit. This bank account is where your SIP auto-debits will come from.

-

4

Search for your chosen fund

In the search bar, type "UTI Nifty 50 Index Fund Direct Growth." Tap on the fund. You will see its NAV, returns chart, fund details, and risk rating. Read the 1-year, 3-year, and 5-year returns. For a Nifty 50 fund, these should be broadly in line with the Nifty 50 index performance.

💡 Confirm it says "Direct" in the fund name — this ensures you are in the zero-commission version. -

5

Tap "Start SIP" and set your parameters

Enter your monthly SIP amount (₹500 minimum for most Nifty 50 funds). Choose a SIP date — the day of the month your installment will be debited. Most advisors recommend picking the 5th or 10th of the month, a few days after your salary credit. Set the duration — "Ongoing" is fine. Tap "Proceed."

-

6

Set up auto-pay (Mandate)

Groww will ask you to set up an auto-pay mandate via UPI, net banking, or NACH. This authorises the app to debit your bank on the SIP date automatically. Approve it from your bank's UPI app or net banking. This is a one-time setup.

-

7

Confirm and you are done

Review your SIP details and tap "Confirm." Your first SIP installment will be invested on your chosen date. You will receive a confirmation email and SMS. After each monthly investment, units are credited to your Groww portfolio. You can track your SIP performance in the app at any time.

✅ Congratulations — you are now an investor. Most people spend years saying "I should start investing." You just did it.

6. What Does ₹500/Month Actually Grow To?

This is the part most people need to see to believe. Here is what different SIP amounts grow to at 12% annual returns (India's historical equity average over 10+ year periods):

| Monthly SIP | 10 Years | 15 Years | 20 Years | Total Invested |

|---|---|---|---|---|

| ₹500 You | ₹1.16 lakh | ₹2.52 lakh | ₹4.99 lakh | ₹60,000 – ₹1.2L – ₹1.8L |

| ₹1,000 | ₹2.32 lakh | ₹5.05 lakh | ₹9.99 lakh | ₹1.2L – ₹1.8L – ₹2.4L |

| ₹2,000 | ₹4.65 lakh | ₹10.1 lakh | ₹19.98 lakh | ₹2.4L – ₹3.6L – ₹4.8L |

| ₹5,000 | ₹11.61 lakh | ₹25.23 lakh | ₹49.96 lakh | ₹6L – ₹9L – ₹12L |

| ₹10,000 | ₹23.23 lakh | ₹50.46 lakh | ₹99.92 lakh | ₹12L – ₹18L – ₹24L |

Assumes 12% CAGR. Historical average for Nifty 50 over 15-20 year periods. Past performance does not guarantee future returns. Educational illustration only.

Try your own SIP calculation

—

ESTIMATED CORPUS

—

TOTAL INVESTED

—

ESTIMATED GAINS

Educational illustration only · Returns not guaranteed · Consult a SEBI-registered advisor before investing

7. 7 Mistakes Beginners Make With SIPs (And How to Avoid Them)

📸 Image Suggestion

")

-

Stopping SIP when markets fall

This is the single biggest mistake. When markets fall, your ₹500 buys more units at lower prices. Stopping your SIP during a crash locks in your loss and removes the averaging benefit. History shows that every market downturn in India has eventually recovered to new highs.

-

Choosing a Regular plan instead of Direct

Regular plans pay 0.5–1% annually to distributors as commission. On a ₹500/month SIP over 20 years, choosing Regular over Direct can cost you ₹1–2 lakh in lost returns. Always search for and select the "Direct Growth" version of any fund.

-

Chasing last year's top performer

A fund that gave 40% last year will not necessarily give 40% next year. Many beginners pick the "top performer" from last year's list and are disappointed when returns normalize. Focus on consistent, low-cost index funds with 5–10 year track records instead.

-

Investing in too many funds at once

Starting five different SIPs of ₹100 each is worse than one ₹500 SIP. Too many funds create confusion, overlap, and over-diversification that cancels out any benefit. Start with one well-chosen Nifty 50 Index Fund. Add a second fund only after 6–12 months.

-

Thinking a low NAV means a "cheaper" fund

A fund with NAV ₹10 is not cheaper or better than one with NAV ₹500. NAV just reflects how long a fund has existed and how much its units have grown. What matters is the fund's expense ratio, tracking error, and long-term performance — not the NAV price.

-

Not increasing SIP when income grows

If you start at ₹500 and never increase your SIP even as your salary grows, you are leaving compounding on the table. A good rule: increase your SIP by 10–15% every year. Most apps have a "SIP Step-Up" or "Auto-increase" feature built in — use it.

-

Redeeming too early for short-term goals

SIP in equity funds is designed for a 5-year+ horizon. Redeeming in 1–2 years means you may sell at a market low and also pay Short Term Capital Gains (STCG) tax of 20% on profits. If your goal is within 3 years, use a debt mutual fund or FD — not an equity SIP.

8. Latest SIP News India — What AMFI Data Says in 2026

To put your ₹500 SIP in context, here is what is happening at the industry level right now. This data shows you are joining one of the fastest-growing retail investment movements in the world.

Business Standard · May 2026

AMFI April 2026: SIP inflows at ₹31,115 crore — dip from March record of ₹32,087 crore amid global uncertainty

hindi.business-standard.com

IANS / Lokmat Times · January 2026

SIP inflows hit record high of ₹31,002 crore in December 2025 — rising 17% year-on-year

lokmattimes.com

Economic Times via Inshorts · January 2026

Monthly SIP inflows have doubled in 3 years to ₹28,202 crore — SIP AUM now exceeds ₹16.52 lakh crore

inshorts.com

BonVista · March 2026

AMFI Feb 2026: 65.72 lakh new SIP registrations in a single month; retail mutual fund accounts at 20.64 crore — Gen Z, women and Tier-2/3 cities driving growth

bonvista.in

What this data tells you: SIP investing is no longer a niche activity in India. It is mainstream. Monthly SIP inflows have more than doubled in just three years, with total SIP assets under management surging to over ₹16.52 lakh crore. The average SIP amount per account is now ₹3,167 — meaning your ₹500 start is well within the typical range of Indian investors.

What this means for you: The infrastructure, regulation, and investor protection systems supporting SIP in India have never been stronger. SEBI's oversight, AMFI's data transparency, and the competition among fund houses to offer the lowest expense ratios all work in your favour as a small investor.

9. Frequently Asked Questions

-

Can I really start SIP with ₹500 in India?Yes, absolutely. Most major Nifty 50 Index Funds on Groww, Zerodha Coin, Paytm Money, and ICICI Direct allow SIPs starting from ₹500/month. Some platforms allow ₹100/month. There is no upper limit. The minimum varies slightly by fund — always check the fund details before starting.

-

What happens if I miss a SIP payment?Nothing serious happens. If your bank account does not have sufficient balance on the SIP date, the debit fails and that month's installment is simply skipped. Your SIP continues next month. The fund house does not penalise you. However, your bank may charge a small bounce fee (₹50–500). After 2–3 consecutive failures, some fund houses may put the SIP on hold.

-

Is SIP safe? Can I lose all my money?SIP in equity mutual funds carries market risk — your invested amount can go down in the short term. However, SIP in a Nifty 50 Index Fund has never delivered negative returns over any 10-year period in India's market history. The risk is significantly reduced with Rupee Cost Averaging, long-term horizon, and choosing a well-regulated fund. Your money is also held in a trust separate from the fund house — even if the AMC closes, your money is safe.

-

How much tax do I pay on SIP returns?For equity mutual funds, if you hold for more than 12 months: the first ₹1.25 lakh of gains per year is completely tax-free (Long Term Capital Gains exemption). Above ₹1.25 lakh, LTCG is taxed at 12.5%. If you redeem within 12 months, Short Term Capital Gains (STCG) is taxed at 20%. For ELSS funds, returns are tax-free on redemption after the 3-year lock-in.

-

Can I stop or change my SIP anytime?Yes. You can pause, increase, decrease, or completely stop your SIP at any time through the app with no penalty from the fund house. There is no lock-in for most open-ended equity funds (except ELSS which has 3 years). Your invested units remain in your account — stopping a SIP does not redeem your units.

-

What is the best app to start SIP with ₹500 in India 2026?For beginners: Groww is the most user-friendly with the cleanest interface. Zerodha Coin is excellent if you already have a Zerodha demat account. Paytm Money and INDmoney are also strong options. All four are free, SEBI-registered, and allow direct mutual fund investments with no commission.

The Bottom Line

If you want to start SIP in India with ₹500, this is the perfect time to begin. Thousands of beginners now start SIP in India with ₹500 using mutual fund apps like Groww to build long-term wealth. When you start SIP in India with ₹500 consistently, you benefit from rupee cost averaging, disciplined investing, and the power of compounding even with a small monthly amount.

According to recent AMFI data, monthly SIP inflows in India have crossed ₹31,000 crore, showing how rapidly retail investors are adopting mutual fund SIP investing. Many young investors now start SIP in India with ₹500 as an affordable way to enter the stock market without large capital. A ₹500 SIP plan India strategy can potentially grow significantly over long periods through compounding and disciplined investing. For beginners, SIP investment for beginners is considered one of the safest and simplest approaches to start mutual fund investing in India while reducing market timing risk through rupee cost averaging.

— Amit K. Sharma, Mint & Print Financial Studies

Post Comment