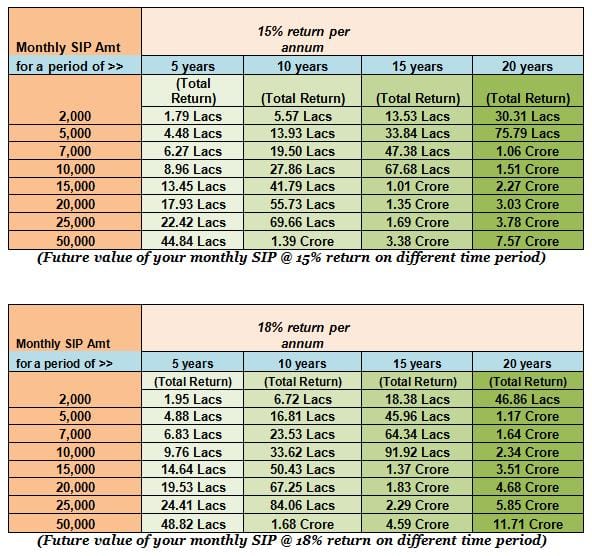

Let’s look at some real scenarios based on historical Indian equity market performance.

Assuming 12% annual CAGR (conservative equity estimate):

| Monthly SIP | 5 Years | 10 Years | 20 Years |

|---|

| ₹500 | ₹40,930 | ₹1,16,170 | ₹4,99,574 |

| ₹2,000 | ₹1,63,712 | ₹4,64,678 | ₹19,98,295 |

| ₹5,000 | ₹4,09,279 | ₹11,61,695 | ₹49,95,738 |

| ₹10,000 | ₹8,18,559 | ₹23,23,391 | ₹99,91,479 |

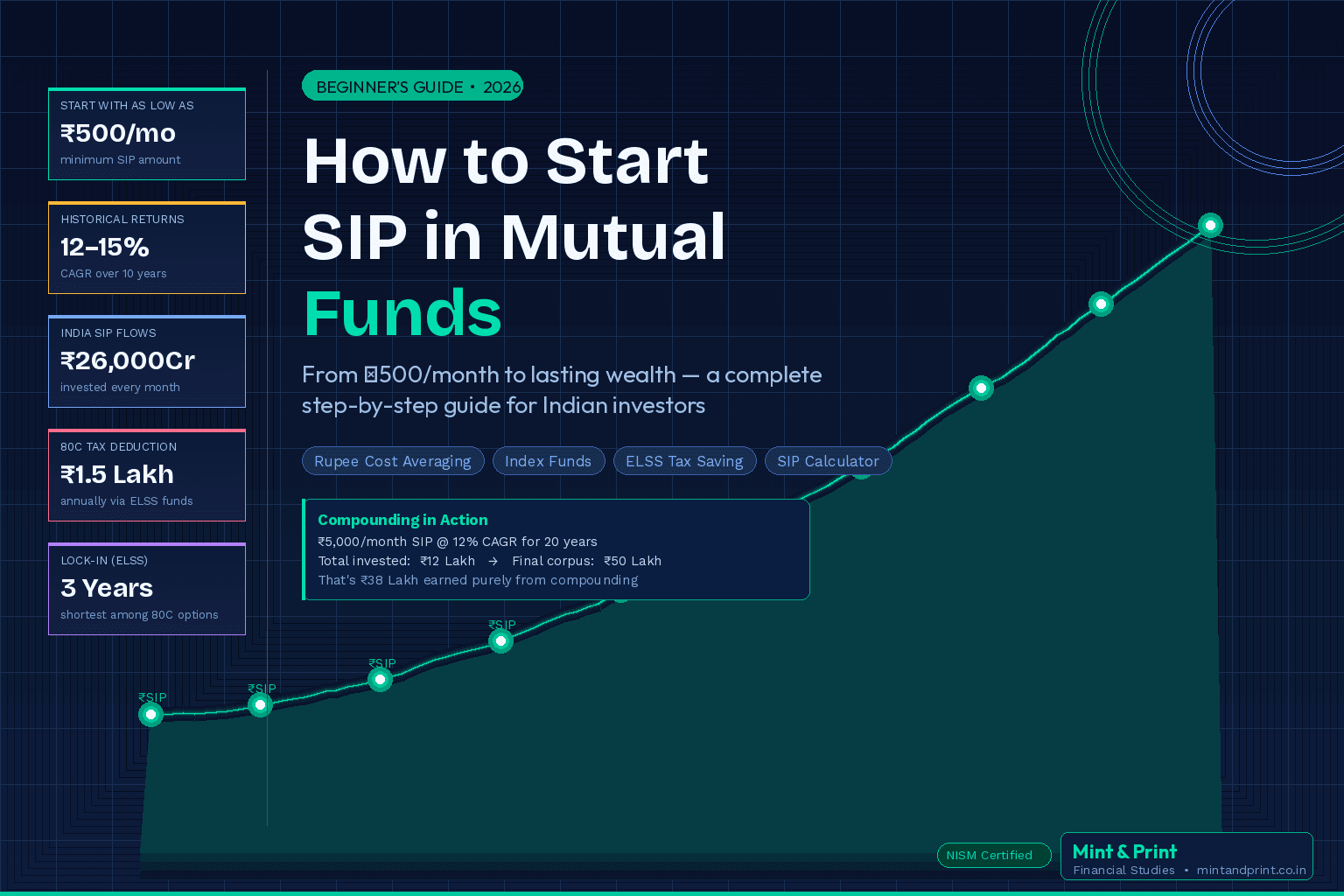

Key insight: ₹5,000/month for 20 years at 12% = nearly ₹50 lakh. Your total investment? Only ₹12 lakh. The rest — ₹38 lakh — is pure compounding.

Note: Past performance does not guarantee future returns. The above figures are illustrative calculations only. Actual returns will vary based on market conditions and fund selection.

SIP Tax Rules Every Beginner Must Know

Mutual fund gains are taxable in India. Here’s a quick breakdown:

Equity Mutual Funds (including Index Funds):

- Gains held for less than 1 year → Short-Term Capital Gains (STCG) taxed at 20%

- Gains held for more than 1 year → Long-Term Capital Gains (LTCG) taxed at 12.5% on gains exceeding ₹1.25 lakh per year

Debt Mutual Funds (as of April 2023 amendment):

- All gains now taxed at your income tax slab rate, regardless of holding period

ELSS Funds:

- Gains after the 3-year lock-in are taxed as LTCG at 12.5% above ₹1.25 lakh

Important: In a SIP, every monthly instalment is treated as a separate investment for tax purposes. So each instalment has its own 1-year holding period clock. Consult a qualified tax advisor for personalised advice.

5 Common SIP Mistakes Beginners Make (And How to Avoid Them)

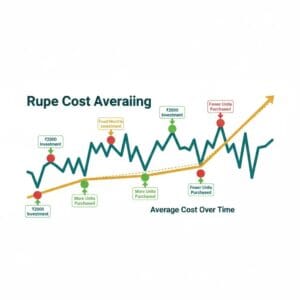

Mistake 1: Stopping SIP when the market falls This is the most costly mistake. A falling market means your SIP is buying more units at a lower price — it’s a sale, not a disaster. Stopping the SIP locks in your losses and misses the recovery.

Mistake 2: Choosing a fund based on last year’s returns Last year’s top-performing fund is often this year’s average performer. Focus on 5–10 year consistency, expense ratio, and fund manager track record.

Mistake 3: Investing in too many funds Beginners often spread ₹2,000 across 8–10 funds thinking they’re diversifying. In reality, you’re just holding the same underlying stocks multiple times. Start with 1–2 funds.

Mistake 4: Not increasing SIP amount over time Your salary will grow. Your SIP should too. A simple rule: increase your SIP by 10% every year. This one habit can double your final corpus.

Mistake 5: Redeeming early for non-emergencies SIP works through compounding — and compounding needs time. Redeeming a 3-year SIP to buy a gadget destroys years of growth. Keep an emergency fund separately so your SIP is untouched.

Key Takeaways

- A SIP invests a fixed amount monthly into a mutual fund, starting from just ₹500

- Rupee cost averaging reduces risk by buying more units when prices fall

- For beginners in 2026: start with Nifty 50 Index Fund + ELSS for simplicity and tax savings

- Always choose Direct Plans to save on expense ratios

- The longer you stay invested, the more powerfully compounding works

- Never stop your SIP during market downturns — those are the best months to accumulate

Frequently Asked Questions (FAQ)

Q1: Can I start a SIP with ₹500 per month?

Yes. Most mutual funds in India allow SIPs starting at ₹500 per month. Some platforms like Groww and Zerodha Coin even offer SIPs starting at ₹100.

Q2: Is SIP safe for beginners?

SIPs in equity funds are market-linked and not risk-free. However, the rupee cost averaging mechanism significantly reduces timing risk. For lower risk, beginners can start with hybrid or large-cap funds.

Q3: How many years should I stay invested in a SIP?

A minimum of 5 years is recommended for equity SIPs, but the real benefits of compounding are most visible after 10+ years. The longer you stay, the better.

Q4: What happens if I miss a SIP instalment?

Missing one month will not cancel your SIP. Most fund houses simply skip that month. If you miss 3 consecutive instalments, your SIP may get paused. You can restart it anytime.

Q5: Can I stop my SIP anytime?

Yes. SIPs are completely flexible. You can pause, stop, or modify your SIP amount at any time without any penalty. There is no lock-in (except for ELSS funds which have a 3-year lock-in).

Q6: Direct plan vs regular plan — which is better?

Direct plans are better for most investors as they have lower expense ratios (no distributor commission), which means higher returns over time. The difference of 0.5–1% annually can compound to a significant amount over 10–15 years.

Conclusion

Starting a SIP is one of the simplest, most powerful financial decisions you can make in your 20s or 30s.

You don’t need a lot of money. You don’t need to understand the stock market deeply. You don’t need to time the market. You just need to start — and stay consistent.

₹500 a month, every month, for 20 years. That’s all it takes to let compounding do the heavy lifting for you.

If you’re ready to deepen your understanding of mutual funds, markets, and financial planning, explore the Study Material section on Mint & Print — we break down every concept from NAV to ELSS to fundamental analysis in plain, simple language.

And if you’re preparing for your NISM certification, check out our Research Lab for structured study guides and market analysis.

This article is for educational purposes only and does not constitute investment advice. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Mint & Print is a NISM-certified financial education platform. We are not SEBI registered investment advisors.

Author: Founder Desk — Amit K Sharma | NISM Certified

Category: Study Material / Indian Market

Tags: SIP, Mutual Funds, Beginners Guide, SIP Investment India, Index Fund, ELSS, Rupee Cost Averaging, Personal Finance India

Internal Links: Study Material, Indian Market, Research Lab

External Links: AMFI India (amfiindia.com), SEBI (sebi.gov.in)

Post Comment