Understanding Asset Classes: Historical Returns, Risk, and the Reality of Risk-Reward

Introduction

Asset classes and their returns and risk form the foundation of every investment decision. Understanding how different assets behave over time is essential for building a balanced and effective portfolio.

Every investment decision ultimately comes down to a simple question: how much risk are you willing to take for the returns you expect?

Different asset classes behave differently over time. Some offer stability but limited growth, while others provide higher returns at the cost of volatility. Understanding this balance is essential for building a resilient financial future.

This article explores the major asset classes, their historical performance, and the relationship between risk and reward—without overwhelming complexity.

The Core Asset Classes Explained

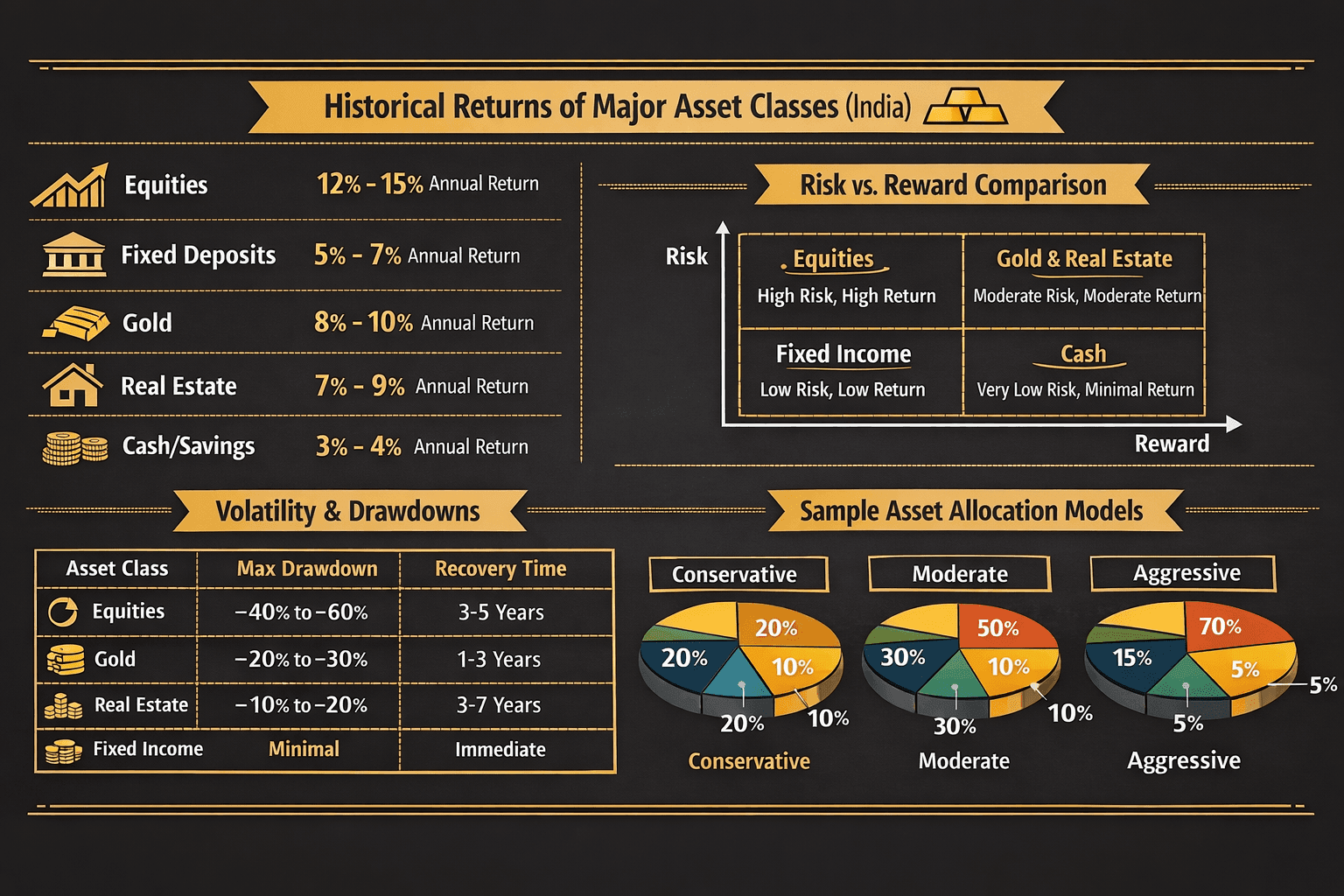

At a broad level, most investment options fall into five primary categories: equities, fixed income instruments, gold, real estate, and cash or savings.

Each of these plays a distinct role in a portfolio. Equities are typically associated with long-term wealth creation. Fixed income instruments provide stability and predictable returns. Gold often acts as a hedge during uncertainty, while real estate offers tangible value and moderate growth. Cash, although the safest, provides minimal returns and is primarily used for liquidity.

Historical Returns: A Long-Term Perspective

Over extended periods, equities have consistently delivered the highest returns among all asset classes. In the Indian context, equities have historically generated annual returns in the range of approximately 12 to 15 percent. However, these returns are not linear and often come with sharp fluctuations.

Fixed deposits and similar instruments, on the other hand, have typically delivered returns between 5 to 7 percent annually. While these returns are lower, they offer stability and capital protection.

Gold has shown moderate performance over time, generally ranging between 8 to 10 percent annually. It tends to perform well during economic uncertainty, inflationary periods, or market stress.

Real estate returns have historically ranged between 7 to 9 percent, though they vary significantly based on location, demand cycles, and economic conditions. Unlike equities, real estate is less liquid and often requires larger capital commitments.

Cash and savings instruments provide the lowest returns, typically around 3 to 4 percent. While they offer safety, they often fail to keep pace with inflation, resulting in a gradual loss of purchasing power.

Understanding Risk Beyond Numbers

Risk is not merely about how much an asset can fall; it is about how it behaves during uncertainty.

Equities, for instance, can experience significant drawdowns. During major market corrections, it is not uncommon for equity markets to decline by 40 to 60 percent. Recovery from such declines can take several years, often between three to five years depending on economic conditions.

Gold, while more stable than equities, can still experience corrections in the range of 20 to 30 percent. However, its recovery period is generally shorter, often between one to three years.

Real estate tends to be less volatile in price movements but can remain stagnant for extended periods. Price declines may range from 10 to 20 percent, and recovery can take several years, sometimes longer depending on market cycles.

Fixed income instruments rarely experience capital loss in traditional forms like fixed deposits, making them one of the safest options. Cash, similarly, does not fluctuate in value but steadily loses purchasing power due to inflation.

The Risk-Reward Relationship

One of the most fundamental principles in investing is that higher returns are usually accompanied by higher risk.

Equities sit at the top of the risk-reward spectrum. They offer the potential for significant long-term growth but require patience, discipline, and the ability to withstand volatility.

Gold and real estate occupy the middle ground. They offer moderate returns with moderate risk and can act as stabilizing components within a portfolio.

Fixed income instruments provide low returns but also low risk, making them suitable for capital preservation and income stability.

Cash represents the lowest risk category but also delivers the lowest returns, often insufficient to build wealth over time.

Why Diversification Matters

No single asset class performs well in all market conditions. Economic cycles, inflation, interest rates, and global events influence each asset differently.

A portfolio heavily concentrated in equities may generate strong returns during bull markets but can suffer during downturns. Conversely, a portfolio focused entirely on fixed income may provide stability but fail to grow meaningfully over time.

Diversification allows investors to balance these dynamics. By combining different asset classes, it is possible to reduce overall risk while maintaining reasonable return potential.

Sample Investment Approaches

An investor with a conservative approach may allocate a larger portion of their portfolio to fixed income instruments, with limited exposure to equities. This ensures stability but limits growth potential.

A moderate investor typically balances equities and debt, aiming for both growth and stability.

An aggressive investor, on the other hand, allocates a significant portion to equities, accepting higher volatility in pursuit of higher long-term returns.

Key Takeaways

The performance of asset classes over time highlights a clear pattern: there is no universal “best” investment. Each asset serves a purpose, and its suitability depends on individual goals, risk tolerance, and time horizon.

Equities are powerful for long-term wealth creation but demand patience. Fixed income offers safety but limited growth. Gold provides protection during uncertainty, while real estate offers tangible value with moderate returns. Cash ensures liquidity but struggles against inflation.

Conclusion

Understanding asset classes is not about memorizing numbers but about recognizing patterns.

Markets will rise and fall. Economic conditions will change. However, the fundamental relationship between risk and return remains constant.

A well-constructed portfolio is not built on chasing the highest returns but on balancing risk, ensuring stability, and aligning investments with long-term financial objectives.

Post Comment